THE AUTHOR:

In the first half of 2025, the euro area recorded 77.7 billion non-cash payments, 7.7% more than during the same period in 2024. The Bank of England and the FCA also found that 75% of surveyed financial firms already use AI, while 41% apply it to internal process optimization.

A banking workflow automation system helps banks process growing transaction and service volumes with fewer manual handoffs, faster approvals, and better operational control.

Payment processing, customer onboarding, lending, contract approvals, and compliance reviews often span core banking platforms, CRM systems, document repositories, spreadsheets, email, and third-party services. Employees have to transfer data, confirm statuses, collect approvals, and resolve inconsistencies across these environments. Each additional handoff increases processing time, operating costs, documentation errors, and the risk of missed controls.

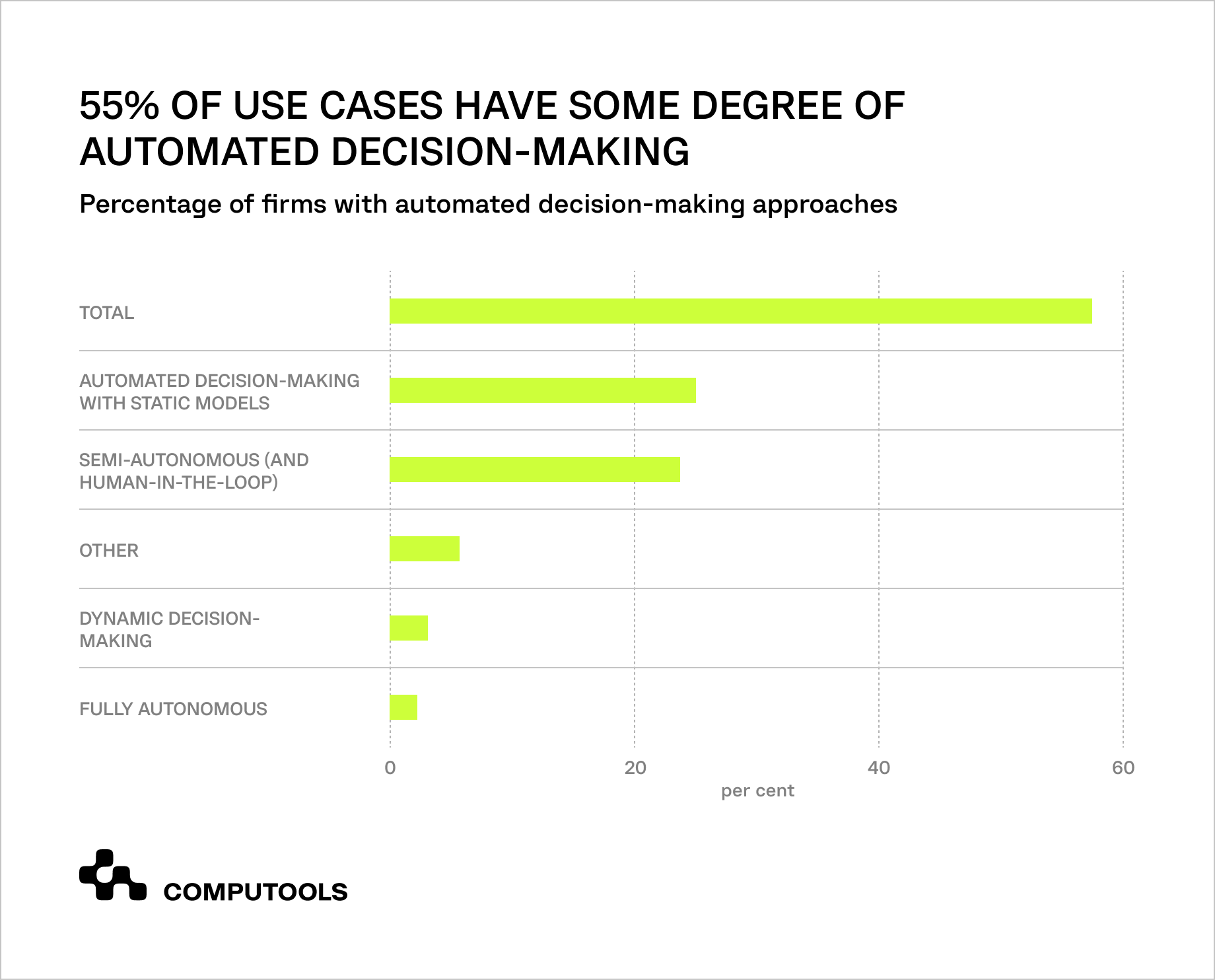

The same Bank of England and the FCA survey found that 55% of AI use cases already involve some automated decision-making, but only 2% are fully autonomous. For banks, the practical model combines rule-based routing, automatic processing of standard cases, human review for exceptions, and a complete audit trail. This structure supports faster operations while preserving accountability for regulated decisions.

How Computools built a banking workflow automation system for credit card issuing

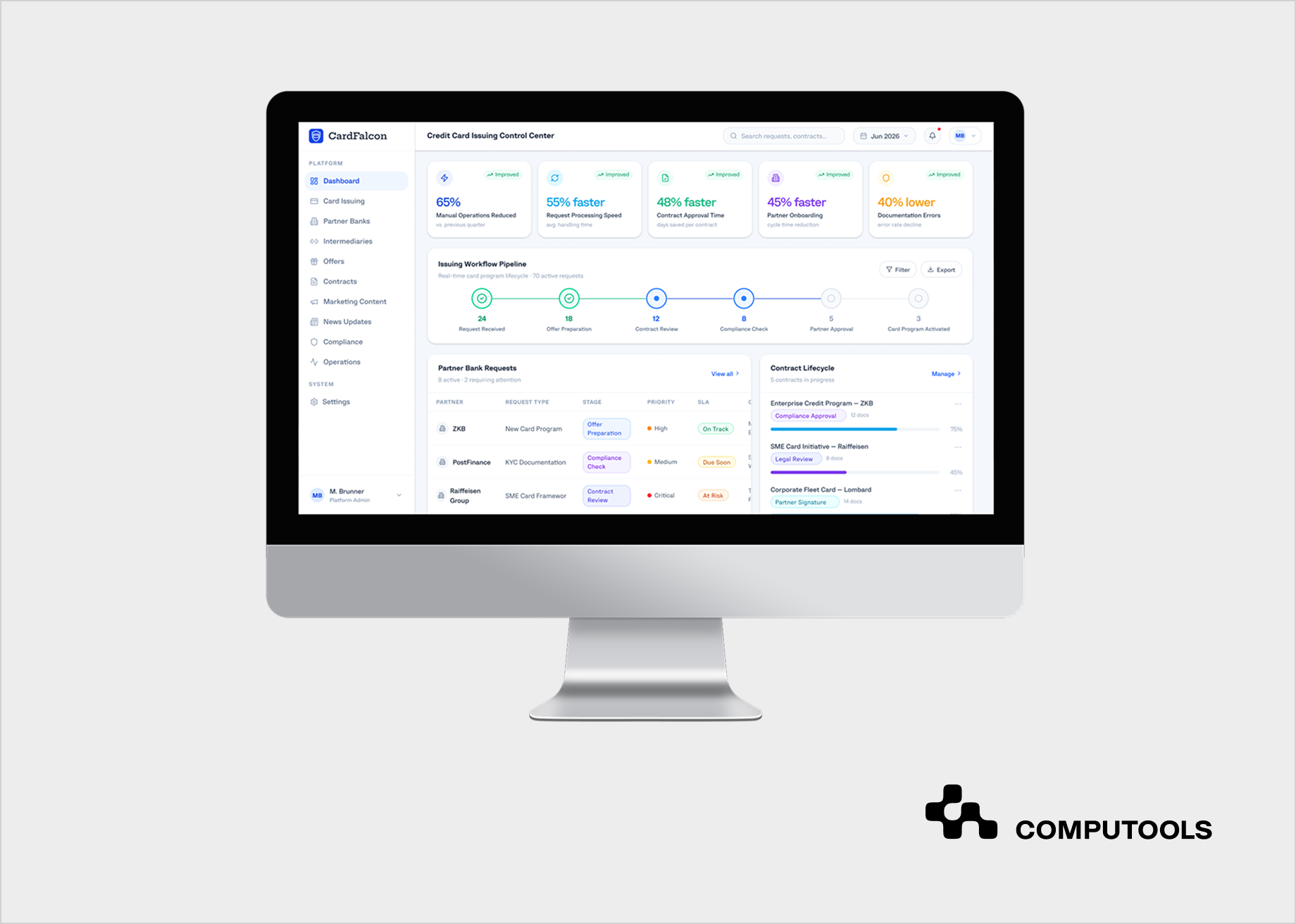

Computools helped build a centralized banking workflow automation system for a Swiss banking institution that needed to digitize credit card issuing operations across partner banks, internal teams, intermediaries, and end customers. The existing process relied on emails, PDFs, spreadsheets, manual approvals, and disconnected internal tools, which slowed request handling and made operational control more difficult.

The project combined banking software development services with backend engineering, partial frontend implementation, CRM-related functionality, and infrastructure setup. The delivered platform consolidated partner communication, offer management, contract approvals, marketing content, news updates, and internal requests into a single controlled environment.

The platform improved partner onboarding by structuring partner data, approval stages, request statuses, and communication across the issuing bank, partner banks, and intermediaries. The same workflow model can support customer onboarding automation in related banking processes.

After implementation, manual operations decreased by 65%, banking requests were processed 55% faster, contract approvals became 48% faster, partner onboarding accelerated by 45%, and documentation errors decreased by 40%.

The bank gained better operational visibility and a more scalable foundation for managing credit card issuing workflows.

How to develop a banking workflow automation system for financial operations step by step

Step 1. Define the operational scope and target KPIs

Start with one financial workflow that creates measurable operational pressure. Strong candidates usually involve high request volumes, repeated manual actions, long approval cycles, frequent rework, or a growing backlog. Trying to automate lending, onboarding, payments, compliance, and servicing in one release makes ownership unclear and delays the first measurable result.

The scope of financial operations automation should be tied to a specific set of baseline and target metrics. These may include average processing time, manual touch rate, straight-through processing rate, approval turnaround time, documentation error rate, SLA compliance, backlog volume, and cost per completed request. The bank also needs to define the process owner, data owner, approval authority, and team responsible for measuring results after launch.

Business and technical teams should document the constraints before architecture work begins. These include existing core systems, integration limitations, regulatory controls, data residency requirements, transaction volumes, expected growth, and acceptable downtime. This information determines whether the first release requires real-time processing, batch synchronization, human approval, or a combination of these.

Step 2. Map the current process and design the target workflow

Document how the selected process operates from the initial request to final completion. The map should capture every trigger, user role, input, document, validation, approval point, system interaction, status change, notification, escalation, and completion condition. The team should combine stakeholder interviews with system logs, sample cases, SLA reports, and direct observation of employee actions because formal procedures often omit the manual workarounds that determine actual processing time.

The analysis should separate value-creating activities from coordination overhead. Value-creating activities include validating data, assessing risk, reviewing documentation, and authorizing a transaction. Coordination overhead includes copying information between systems, locating files, confirming ownership of requests, checking approval status, sending reminders, and resolving conflicting records. A complete banking business process map shows which steps require professional judgment and which exist only because systems and teams do not exchange information reliably.

Each step should then be evaluated against a consistent set of criteria:

• average and maximum processing time;

• number of manual touchpoints;

• frequency of returns and repeated checks;

• systems and data sources involved;

• approval dependencies;

• exception frequency;

• SLA exposure;

• error and rework rates;

• control and compliance requirements.

This assessment helps identify initial automation candidates by highlighting repetitive steps governed by clear rules that are suitable for removal or automation, while reserving risk-sensitive decisions for human oversight. The target workflow should specify the standard route, alternatives, and exception scenarios before development. It also requires explicit ownership, with each workflow status assigned a role, an entry condition, permitted actions, an SLA, and an exit condition. Escalation rules should cover cases such as user inaction, integration failures, missing data, or conflicting validation results, ensuring these cases don’t remain in undefined states and providing a clear resolution mechanism for operations teams.

For CardFalcon, process discovery revealed that requests, offers, contracts, communications, and content updates were handled via email, PDFs, spreadsheets, and disconnected internal tools. Partner banks, intermediaries, and internal teams followed separate coordination paths, limiting visibility and increasing manual follow-up. The target workflow consolidated these activities into a single environment, with structured statuses, approval stages, role-based actions, and shared operational records. This redesign created the foundation for faster request handling, contract approvals, and partner onboarding.

Step 3. Create a controlled data foundation

Define the information the workflow needs before selecting databases, integration patterns, or automation tools. The data model should reflect the real operational process and include customers, partner institutions, accounts, products, requests, offers, contracts, documents, approvals, users, roles, workflow statuses, and audit events. Each entity needs a unique identifier, clear relationships, required fields, validation rules, and an accountable data owner.

The team should also document how records move through their lifecycle. A request may begin as a draft, proceed through validation and approval, return for correction, and end as completed, rejected, or canceled. The system must define which status transitions are permitted, which roles can initiate them, and what data or documents are required before the workflow can continue. These controls prevent incomplete cases from progressing and ensure operational status is consistent across departments.

The data engineering scope should determine how information enters, changes, and leaves the platform.

This includes:

• source-to-target field mapping;

• API, event, and batch ingestion;

• schema and format validation;

• duplicate detection and record matching;

• reference-data standardization;

• synchronization frequency;

• data lineage;

• reconciliation procedures;

• quality monitoring;

• retention and deletion rules.

A source-of-truth model is vital when the same data exists across core banking, CRM, storage, and third-party services. The software architecture must specify who owns each record and how conflicts are resolved. Without these rules, automation may spread inconsistent data as employees manually correct records.

The platform should keep historical data and record influences on decisions. Values like approval limits, customer info, contract terms, workflow rules, and risk classifications change over time. Versioned records help reconstruct data at review time and clarify the reasons for decisions.

The data layer also needs operational safeguards. Validation errors should create actionable exceptions. Silent rejection and record corruption must be prevented. Failed imports, unmatched identifiers, synchronization delays, and duplicate events must be visible through monitoring and resolution queues. These controls give operations teams a clear way to restore data consistency without relying on engineering support for every failed transaction.

For financial workflows that depend on high-volume data and time-sensitive calculations, see our guide on how to build an investment management platform with real-time market data.

Step 4. Design a modular platform architecture

Translate the target workflow and data model into a system architecture that supports evolving rules, new products, additional user groups, and higher transaction volumes. The platform should separate process orchestration, business logic, integrations, data storage, user interfaces, notifications, analytics, and audit logging. This prevents one workflow change from affecting unrelated modules and reduces the cost of future expansion.

A financial workflow automation system typically includes several core layers:

• workflow orchestration for task sequencing and status transitions;

• a business rules engine for validations, routing, and approval thresholds;

• case management for exceptions and manual review;

• an integration layer for internal and external systems;

• operational databases and document storage;

• role-based user interfaces;

• notification and escalation services;

• audit logging, monitoring, and reporting.

The workflow engine should centrally control process state. Distributed status logic is harder to trace and maintain across interface components and integration scripts. It needs to track the current stage, completed actions, assigned user, pending dependencies, SLA deadlines, and permitted next steps. Long-running workflows should preserve state across user actions, external responses, and scheduled checks without requiring a restart.

Business rules should remain separate from the core workflow where possible. Approval limits, routing conditions, required documents, escalation periods, and exception criteria may change more frequently than the application architecture. A configurable rules layer allows authorized teams to update operational logic through controlled testing, versioning, and approval. This removes the need for a full software release after every policy change.

The architecture must define how modules communicate, choosing synchronous APIs for immediate responses, such as account validation, and asynchronous messaging for long-running operations, updates, and interactions with temporarily unavailable systems. Message queues, idempotency, retries, and dead-letter handling help prevent duplicate actions or lost requests.

Scalability depends on workload patterns, user and request estimates, peak periods, document size, API limits, and growth. Stateless services scale horizontally; stateful ones need consistency controls, backups, and recovery plans.

Operational resilience should be planned early, with clear definitions of availability, recovery times, timeouts, fallback routes, and degraded modes. If an external provider fails, the system may pause, route for manual review, or retry. Silent failures must be blocked and logged.

Observability is another architectural requirement. Technical teams need centralized logs, metrics, distributed tracing, integration status, queue depth, error rates, and processing latency. Operations teams need a different view: blocked cases, overdue tasks, failed validations, unavailable services, and workflows approaching SLA limits. Separating technical monitoring from operational monitoring gives each team actionable information.

For CardFalcon, Java, Spring Framework, and Spring Boot formed the backend foundation for requests, offers, contracts, user roles, approval flows, and communication logic. Angular and TypeScript supported operational interfaces; PostgreSQL stored structured records; Salesforce handled CRM-related data; and Docker provided consistent environments across development, testing, and deployment. This modular architecture enabled the bank to manage multiple participant groups and operational flows on a single, controlled platform.

Step 5. Standardize document intake and lifecycle management

Banking workflows depend on documents that arrive from multiple channels and move through several review stages. Applications, contracts, identity records, financial statements, supporting evidence, product terms, approval forms, and customer notices may be uploaded through portals, received by email, generated internally, or imported from third-party systems. Without a controlled intake process, employees spend time locating files, checking versions, and confirming whether a document belongs to the correct customer or request.

The first task is to define a document taxonomy. Each document type should have:

• a unique classification;

• mandatory metadata;

• an associated customer, account, partner, or case;

• an owner;

• validation requirements;

• permitted formats and size limits;

• an approval status;

• retention and deletion rules;

• access restrictions;

• expiration or renewal conditions.

A structured banking document management layer should connect each file to the workflow that depends on it. For example, a contract should remain linked to the relevant partner, offer, approval history, and request status. This gives employees access to the current document context without having to search across shared folders, inboxes, and separate platforms.

Document intake should include automated validation before a case moves forward. The platform can verify whether mandatory files are present, confirm file type and completeness, check metadata against customer or request records, and identify duplicates or expired documents. Failed checks should create a visible exception with a clear reason and an assigned owner. The workflow should block further processing until the issue is resolved.

Version control is crucial for contracts, terms, and evidence of compliance. The system must store previous versions, record who uploaded or modified files, and track which version was used for approvals or communications. Approved documents should be locked against editing, with new review cycles for updates.

The workflow should clearly define document statuses, including draft, received, pending validation, incomplete, under review, approved, rejected, expired, and archived. Each status has specific transition rules and actions, such as requesting more info for ‘incomplete’ or blocking processing for ‘expired’. For high-volume processes, document intelligence reduces manual data entry by using OCR and extraction models to capture key fields. Data must meet validation thresholds before records are updated; low-confidence results require review.

Access control applies at both the document and case levels, granting permissions to internal teams, partners, intermediaries, and admins to view, upload, approve, or replace files. Sensitive documents should be encrypted, logged, and protected from bulk export or sharing. The platform also needs to be monitored for operational document risks.

Dashboards should show missing files, expired documents, validation failures, pending approvals, duplicate uploads, and cases blocked by incomplete evidence. This gives supervisors visibility into the document-related causes of delays and allows teams to resolve bottlenecks before they affect SLA performance.

For CardFalcon, contracts, offers, marketing materials, and news updates were consolidated into one controlled environment. Contract lifecycle tracking, approval stages, and centralized content management reduced reliance on email, improved document consistency, and gave teams a clear view of current statuses.

Step 6. Configure business rules, approvals, and exception handling

Translate operational policies into explicit system logic. The rules should determine which requests can proceed automatically, which require additional validation, who can approve them, and what happens when data is missing or results conflict. This creates consistent processing across teams and reduces dependence on individual interpretation.

The banking process automation software should support several rule types:

• field and document validation;

• eligibility checks;

• approval thresholds;

• role-based routing;

• maker-checker controls;

• SLA timers;

• escalation conditions;

• reassignment rules;

• cancellation and resubmission;

• manual overrides with recorded justification.

Rules should remain separate from interface code and, where possible, be managed through version-controlled configuration. Approval limits, required documents, routing conditions, and escalation periods may change after regulatory updates or internal policy reviews. A configurable rules layer allows the bank to update operational logic without rebuilding the full application.

Each decision needs a clear input, output, and reason code. The platform should record which rule was applied, which data triggered the result, which version of the rule was active, and whether a user changed the automated outcome. This gives compliance and operations teams a reproducible decision history and simplifies audit preparation.

Approval workflows should reflect actual authority levels. A request may require a single approver, sequential approval, parallel review by several teams, or additional authorization for amounts or risks above a defined threshold. The system should prevent unauthorized users from changing approval states and enforce segregation of duties, ensuring that the same employee cannot both initiate and approve the same action.

Exception handling requires its own workflow design. The team should define how the platform responds to:

• incomplete or inconsistent data;

• duplicate requests;

• failed validations;

• unavailable external services;

• expired approvals;

• conflicting rule results;

• missed SLA deadlines;

• rejected or returned cases;

• failed notifications or data transfers.

Each exception must create a case with the owner, priority, deadline, error context, and allowed resolution. Repeated failures should not trigger unlimited retries to prevent duplicate records. Retry limits, idempotency controls, dead-letter queues, and manual pathways keep failures contained and traceable. The platform must support manual intervention. Employees may need to correct data, reassign cases, request documents, or override decisions. These actions require role restrictions, reason codes, and audit logs. Supervisors should monitor override frequency and workflows with excessive exceptions or manual decisions.

Step 7. Integrate core banking systems and external services

List every system that creates, validates, stores, or updates workflow data. Depending on the selected process, the platform may need to connect with core banking, CRM, payment infrastructure, identity verification providers, KYC and AML tools, document repositories, accounting systems, notification services, and regulatory reporting platforms. Each integration should have a defined purpose, data owner, authentication method, response-time requirement, and failure policy.

The integration architecture should support several communication patterns. Synchronous APIs are suitable for operations that require an immediate response, such as retrieving a customer profile, checking an account status, or validating a payment limit. Asynchronous messaging is more reliable for long-running workflows, high-volume updates, notifications, and processes that depend on several systems. Scheduled batch transfers may still be necessary when legacy platforms cannot exchange data in real time.

A fintech software development project should define a clear data contract for every connection. The contract needs to specify field names, formats, mandatory values, validation rules, error codes, versioning, and ownership. Without standardized contracts, changes in one system may silently break downstream workflow logic or create inconsistent records across operational platforms.

The integration layer should also protect workflows from temporary service failures.

Relevant controls include:

• idempotency keys to prevent duplicate processing;

• message queues for reliable delivery;

• timeout and retry policies;

• dead-letter queues for unresolved messages;

• circuit breakers for unavailable services;

• schema validation;

• reconciliation jobs;

• integration health monitoring.

Retry behavior in finance needs control. Repeating failed reads might be harmless, but duplicate transactions can occur if payments or account updates are repeated. Operations should be classified as read-only, repeatable, or non-repeatable, with recovery logic aligned to their financial impact.

The platform must maintain traceability. Logs should record data receipt, transformation, rejection, resending, or transfer. A shared correlation ID links workflow events, API calls, database changes, and external responses, aiding root cause analysis and delaying understanding. Monitoring should address both business impact and technical availability. A service might be online but return incomplete data, process slowly, or have high error rates. Dashboards should track failed exchanges, queue depth, latency, rejected records, sync delays, and blocked workflows.

For CardFalcon, the team integrated CRM-related functionality, backend modules, Angular interfaces, and the PostgreSQL data layer into a single operational environment. Partner information, communication history, offers, contracts, requests, and workflow statuses could flow through a coordinated system that replaced separate tools. This gave internal teams and partner institutions more consistent access to operational data and reduced manual reconciliation between channels.

For a closer look at API architecture, third-party dependencies, and compliance controls in customer-facing financial products, read our guide on how to build a fintech mobile app with secure banking integrations.

Step 8. Embed compliance controls and auditability into the workflow

Compliance requirements should be embedded directly in the workflow logic and executed before a case advances. The platform needs to enforce mandatory data, required documents, approval segregation, review deadlines, and escalation rules before a case can move to the next status.

Compliance workflow automation should determine which controls apply to each request based on product type, customer category, transaction value, jurisdiction, risk level, and operational role. A standard case may proceed after automated validation, while a higher-risk or incomplete request should be routed to an authorized employee with the relevant evidence already attached.

The system should record the full context behind every decision, including:

• the rule or policy applied;

• the input data used;

• the rule version active at the time;

• the result of each validation;

• the employee or system that performed the action;

• the reason for approval, rejection, return, or escalation;

• all subsequent changes to the case.

This audit trail should be append-only and protected from unauthorized modification. Updating a request, document, approval status, or business rule must create a new recorded event and preserve the previous state. This allows internal audit and compliance teams to reconstruct how the case progressed and which information was available when a decision was made.

Segregation of duties should be enforced technically to prevent employees from initiating and approving restricted actions, changing approval limits, or bypassing reviews. Approval roles can be set by role, amount, product, business unit, and risk. Human review remains essential for conflicting info, policy exceptions, high risk, or professional judgment. The workspace should display checks, unresolved issues, documents, decisions, and actions to reduce repeated investigations and ensure consistency.

Workflow management should track deadlines, with SLA timers for review duration, reminders, and escalations. Dashboards should show pending reviews, aging cases, overrides, control failures, and high exception workflows, helping teams identify process issues early.

Step 9. Build role-based workspaces and secure access controls

Design each workspace around the decisions a user needs to make. Operations specialists, supervisors, compliance officers, partner institutions, intermediaries, and system administrators interact with the same process but require different data, actions, and levels of visibility. A generic interface usually forces users to navigate irrelevant records and increases the risk of unauthorized actions.

Each role should have a defined set of permissions for:

• viewing customer, partner, and request data;

• creating or editing records;

• uploading and approving documents;

• changing workflow statuses;

• assigning or reassigning cases;

• approving exceptions;

• exporting information;

• modifying rules or system configuration.

Permissions should combine role-based access control with contextual restrictions based on factors such as business unit, jurisdiction, product, partner institution, case ownership, or transaction value. For example, a partner-bank user may view requests linked to their organization but shouldn’t access another institution’s contracts, communication, or history.

The interface must show all required context for decision-making: request details, related documents, previous actions, validation results, status history, deadlines, and next steps. Task queues should be prioritized by SLA, risk, value, or exception. Clear validation messages and disabled unauthorized actions reduce errors and avoid consulting other systems.

Administrative functions need stricter controls than routine cases. Changes to approval thresholds, user permissions, workflows, and integrations can impact many operations. These should require elevated authorization, confirmation, change logs, and approval by a second administrator.

The cybersecurity services scope should cover multifactor authentication, encryption in transit and at rest, segregation of duties, privileged access management, secrets protection, session controls, vulnerability management, and security event monitoring. Sensitive actions such as bulk exports, manual overrides, permission changes, and repeated failed access attempts should generate alerts and remain visible in the audit trail.

Security testing should include authorization checks at both the interface and API levels. Hiding a button does not prevent a user from calling the underlying endpoint directly. Automated tests should verify that users cannot retrieve, update, approve, or export records outside their assigned permissions. Penetration testing and dependency scanning should be completed before production rollout and repeated after material architectural changes.

For CardFalcon, the design process included user personas, site structure, wireframes, and interfaces for bank staff managing partner communication, offers, contracts, requests, and workflows. Angular and TypeScript supported role-specific screens, with backend logic managing roles and approvals. The architecture ensured access control, security, and support for multiple participant groups in regulated banking workflows.

Our guide to implementing enterprise cybersecurity for financial services companies explains how centralized monitoring, access controls, vulnerability management, and incident response support regulated financial operations.

Step 10. Test, pilot, and scale the platform against operational KPIs

The testing process should cover complete business scenarios across screens, APIs, integrations, roles, and workflow states. The team needs to verify how a request moves through intake, validation, approval, exception handling, and final completion. Test data should include standard cases, missing information, invalid documents, duplicate submissions, rejected approvals, unavailable integrations, expired tasks, unauthorized actions, and conflicting rule results.

The test plan should combine:

• unit and integration testing;

• end-to-end workflow testing;

• role and permission testing;

• data migration validation;

• performance and load testing;

• failover and recovery testing;

• security testing;

• user acceptance testing.

Each scenario requires an expected workflow state, a system response, a responsible role, and a recovery path. For example, an unavailable external service should pause or reroute the case without losing data, while a repeated submission should be identified before it creates a duplicate operational record.

The initial release should cover a limited, representative scope, such as a single product, partner group, branch, or operational team. A controlled pilot allows observation of exception patterns, employee behavior, integration issues, and bottlenecks before they have a broader impact on the platform. Pilot acceptance criteria must be set before launch. Technical stability alone isn’t enough if users rely on email/spreadsheets or if new workflows increase manual reviews. The bank should compare pilot results with the baseline set at the start.

The banking operations management software should provide operational dashboards for:

• average processing time;

• manual touch rate;

• straight-through processing rate;

• approval turnaround time;

• exception volume;

• SLA compliance;

• rework and return rates;

• backlog by team and status;

• integration failures;

• documentation errors;

• cost per completed request.

These metrics reveal if the platform reduces operational effort or just shifts it to another team. They help identify workflows that need rule changes, integrations, interface upgrades, or improved data validation before broader deployment. The rollout plan should focus on the process’s proven value. Once the pilot stabilizes and KPIs are met, the bank can expand to more products, workflows, user groups, and regions, reusing data models, integrations, security, and monitoring, while maintaining process-specific rules.

CardFalcon was delivered in short iterations covering backend logic, offer and contract workflows, partner communication, operational interfaces, database integration, and deployment infrastructure. Regular reviews and checkpoints helped the client validate approval logic, user flows, and technical dependencies before broader rollout. This phased approach reduced implementation risk and gave the bank a controlled path from initial validation to measurable operational improvement.

Launch your banking workflow automation system within 1–3 months instead of years, and turn manual banking processes into a strategic advantage powered by intelligent automation.

What implementation risks can undermine banking workflow automation?

Workflow automation reduces manual effort, speeds up processing, and enhances control, but poor implementation can limit benefits. Risks include legacy integration, incomplete exception handling, lack of traceability, and automation that creates downstream bottlenecks.

Challenge 1: Legacy integration can preserve existing fragmentation

Banks rely on diverse core systems, CRM systems, document storage, payment systems, and internal apps built at different times and with different data models. Some support modern APIs, others use batch files or manual exports. Replacing everything in one go is costly, risky, and complex.

Effective bank workflow management requires an integration layer that standardizes data exchange without forcing all legacy systems into a single architecture. API adapters, event queues, schema mapping, and reconciliation help maintain existing systems while providing consistent data access.

Risks increase when data ownership and failure protocols are unclear, leading employees to manually verify records, check statuses, and fix inconsistencies, creating a new interface without easing overall coordination.

Challenge 2: Incomplete exception logic can create new manual backlogs

Standard cases are easiest to automate, but missing documents, unavailable services, duplicate requests, expired approvals, conflicting results, and unusual customer situations increase operational load. A workflow based only on the expected route will push these cases into email, spreadsheets, or support queues afterward.

Automated banking processes need clear exception paths with owners, priorities, SLAs, resolution actions, and escalation rules.

The platform should differentiate technical failures from cases needing operational or compliance judgment, and prevent retries, duplicates, or status changes without clear next steps. Business rules present additional risks. Approval limits, routing, documents, and escalation policies change over time. Embedded rules in code make updates dependent on releases. Versioned configuration, effective dates, testing, and rollback procedures enable the bank to update logic without disrupting workflows.

Challenge 3: Weak traceability can undermine KYC and compliance decisions

KYC processes combine customer data, identity documents, screening results, risk classifications, and employee decisions from multiple systems. Automation can reduce repetitive checks, but every result must connect clearly to the data, rule, and user action that produced it.

A reliable KYC workflow automation should validate information, trigger checks, identify missing evidence, assign review levels, and preserve decision history. Higher-risk or conflicting cases should enter controlled queues with all relevant documents and unresolved issues. The platform must support periodic and event-driven reviews, as changes in customer info or behavior may require reevaluation before scheduled reviews. Without automated triggers and deadlines, teams rely on manual reminders and spreadsheets, risking inconsistent or overdue reviews.

Challenge 4: Partial automation can shift bottlenecks into later stages

Lending workflows combine application intake, document review, eligibility checks, risk assessment, underwriting, approvals, contract generation, and disbursement. Automating the front end may increase applications without improving underwriting or approval capacity.

Loan processing automation should cover the entire process. Standard applications pass data validation and eligibility checks automatically, while complex cases are reviewed as needed. The platform must link application data, documents, decisions, approval history, and final agreements. Post-launch, measuring workload and queues is vital. Faster intake without increased review capacity deepens backlogs. Banks need visibility into processing times, queue age, exception volume, reviewer capacity, and return rates to ensure automation eases workload without causing new bottlenecks.

For a detailed view of borrower verification, credit assessment, KYC, and payment workflows, see our guide on how to build a peer-to-peer lending platform for emerging markets.

Why financial institutions choose Computools

Computools approaches digital transformation in banking through phased delivery, measurable KPIs, and validation before full rollout. Its financial software development services cover workflow design, integrations, UX, analytics, and launch support, helping banks reduce execution risk and reach operational value faster.

| Delivery stage | What Computools does | Proof point |

| Discovery and KPI definition | Maps workflows, data flows, user roles, bottlenecks, and compliance dependencies | Custom banking solutions have delivered an average 35% increase in operational speed |

| Product and architecture design | Defines workflow logic, data models, integrations, UX design, security controls, and the ROI roadmap | Delivery is supported by 250+ experts and experience across 10+ banking projects |

| Pilot delivery | Launches one high-value workflow for a selected process, product, or user group | Banking software solutions can be launched within 1–3 months |

| Phased implementation | Delivers functionality through short iterations and clear checkpoints | CardFalcon reduced manual operations by 65% and accelerated request processing by 55% |

| Rollout and optimization | Tracks adoption, exceptions, processing time, risk exposure, and growth KPIs | CardFalcon reduced documentation errors by 40%, while Caribbean Bank increased market share among customers aged 18–30 by 12% |

Computools applies workflow automation in banking across onboarding, approvals, document handling, compliance, and servicing. Web development services support role-based operational portals and management dashboards, while AI development can reduce manual work in document processing, case summarization, and exception prioritization.

CardFalcon demonstrates the operational side of this model: one platform connected with partner communication, contracts, offers, approvals, and internal requests.

For Caribbean Bank, platform engineering, Visa integration, and redesigned web and mobile experiences drove a 12% increase in market share among customers aged 18–30.

Moblet demonstrates how cross-platform development, secure transaction logic, and backend engineering can support the launch and adoption of a consumer financial product.

This gives banks a controlled path from one validated workflow to broader banking operations automation, with each expansion tied to confirmed KPI results.

Ready to reduce manual processing and automate high-friction banking workflows? Contact our financial software experts at info@computools.com.

To sum up

Banks cannot scale financial operations while approvals, documents, compliance checks, and exceptions remain split across disconnected systems and manual handoffs. Effective banking automation solutions create one controlled operating model for data, decisions, and accountability, helping institutions reduce processing costs, shorten cycle times, strengthen auditability, and expand capacity through a clear roadmap to ROI.

For a deeper look at identity verification, document validation, biometric checks, sanctions screening, and compliance automation, see our guide on how to develop an automated KYC verification system.

Computools

Software Solutions

Computools is an IT consulting and software development company that delivers innovative solutions to help businesses unlock tomorrow.