THE AUTHOR:

In light of external partnerships forming a core part of revenue streams, compliance, and operational workflows, banks and fintech companies face a strong need to develop banking partner onboarding software. Juniper Research predicts a huge increase in open banking API calls, growing from 137 billion in 2025 to 722 billion in 2029. The number of open banking users will grow from 183 million to more than 645 million in the same period. This shifts expectations for banks as partner onboarding becomes a front-office function.

As more platforms start to include payment methods, loans, cards, accounts, and other financial services, the value of embedded finance is projected to grow from USD 145.03 billion in 2025 to USD 193.27 billion in 2026, according to Fortune Business Insights. In this environment, banks require more robust banking ecosystem onboarding solutions that can approve partners quickly without losing control over KYB, contract status, compliance evidence, API credentials, revenue rules, and operational limits.

Regulation adds another layer. The EU Digital Operational Resilience Act entered into application on January 17, 2025, and requires financial entities to withstand, respond to, and recover from ICT disruptions such as cyberattacks and system failures. This matters for third-party onboarding in banking because every API-connected partner becomes part of the bank’s operational risk environment.

To develop banking partner onboarding software properly, banks need more than document upload forms. They need a bank partner management platform that connects due diligence, approval routing, API provisioning, contract control, risk scoring, monitoring, and lifecycle governance.

This article explains how to design that system, what technical decisions matter, how Computools’ CardFalcon case proves the business value, and which architecture choices reduce risk before the ecosystem scales.

Essential features of a banking partner onboarding platform

A partner onboarding platform for banks needs to control how partners are verified, approved, integrated, monitored, and managed after activation. The table below shows the core features banks should plan before development starts.

| Feature | What it should do | Business value |

| Partner profile management | Store legal entity data, business model, ownership details, product requests, operating countries, expected volume, and internal owner. | Gives teams one reliable partner record instead of scattered CRM notes, files, and email threads. |

| Document collection and validation | Collect KYB documents, licenses, ownership evidence, contracts, technical files, and compliance forms with expiry tracking. | Reduces missing documents, repeated requests, and manual follow-ups. |

| KYB and beneficial ownership review | Support entity verification, ownership structure checks, UBO records, sanctions screening, and review status tracking. | Improves compliance visibility before partners receive access to banking products or APIs. |

| Compliance workflow automation | Route cases to compliance, legal, risk, product, security, and operations teams based on partner type and risk level. | Shortens approval cycles and keeps accountability clear across departments. |

| Risk scoring and exposure controls | Assign partner risk levels based on geography, product type, business model, volume, ownership complexity, and screening results. | Connects onboarding speed with risk control, transaction limits, API scopes, and review frequency. |

| Contract lifecycle tracking | Manage contract drafts, approval status, signed agreements, renewal dates, commercial terms, and access conditions. | Prevents production access before legal and commercial requirements are complete. |

| API access management | Control sandbox access, production credentials, API scopes, rate limits, webhook settings, and access suspension. | Protects banking IT infrastructure while allowing approved partners to integrate faster. |

| Partner communication and notifications | Send automated updates about missing documents, review status, approval steps, testing results, and activation milestones. | Reduces support pressure and keeps partners informed without manual status emails. |

| Audit logs and reporting | Record decisions, approvals, rejected cases, document changes, access changes, and user activity. | Supports audits, compliance reviews, incident investigation, and management reporting. |

| Monitoring and lifecycle management | Track active partners, API usage, renewal dates, risk changes, incidents, support requests, and offboarding steps. | Keeps partner governance active after launch instead of ending control at activation. |

How Computools helps develop banking partner onboarding software: CardFalcon case study

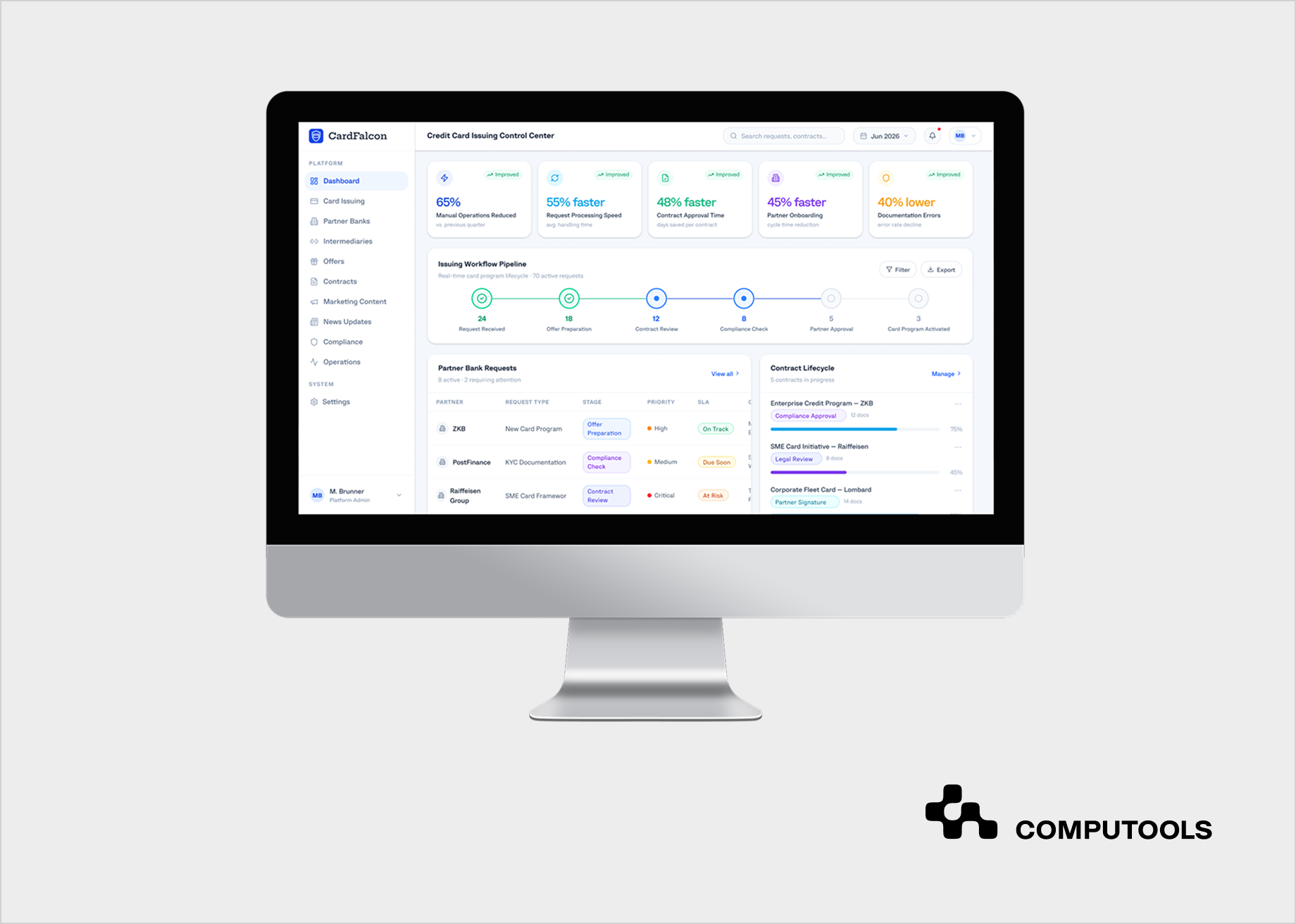

CardFalcon was built for a Swiss banking institution operating in banking and payments. The client’s credit card issuing process connected the issuing bank, partner banks, intermediaries, internal teams, and end customers inside one B2B2C service chain. The client needed one environment to manage communication, offers, contracts, marketing materials, news updates, and internal operational workflows.

Business challenge

Before the project, issuing operations depended on emails, PDFs, manual approvals, spreadsheets, and disconnected tools. Partner banks, intermediaries, and internal teams worked through separate channels, which slowed request handling and weakened visibility. Offers, contracts, and marketing updates were spread across different systems, increasing the risk of outdated information, duplicate work, and documentation errors.

This challenge is close to what banks face when they build a partner onboarding platform for banks. When partner documents, contracts, approval decisions, API permissions, and operational records live in different systems, onboarding speed improves only on the surface. Risk still remains scattered.

Computools solution

Our team engineered a centralized banking platform that created one operational environment for bank employees, partner banks, intermediaries, product teams, and marketing teams. The solution included credit card issuing workflow automation, offer management, contract lifecycle tracking, marketing and news management, and structured operational request handling.

The platform was built with Salesforce, Java, Spring Framework, Spring Boot, Angular, TypeScript, PostgreSQL, and Docker. Salesforce supported the CRM layer. Java, Spring, and Spring Boot formed the backend foundation for requests, offers, contracts, roles, approvals, and communication. Angular and TypeScript supported operational interfaces, while PostgreSQL stored partner-bank data, contracts, offers, workflow statuses, operational history, and activity records. Docker supports containerized deployment and consistent release environments.

Business result

After implementation, our client saw such improvements:

- manual operations decreased by 65%;

- banking request processing shortened by 55%;

- contract approvals became 48% faster;

- partner onboarding took 45% less time;

- documentation errors decreased by 40%.

For banking API partner onboarding, these results show the following. When workflows, contracts, partner records, access rules, and operational history are connected, the bank can scale partnerships without turning compliance and operations into a bottleneck.

How to develop banking partner onboarding software as an ecosystem control layer

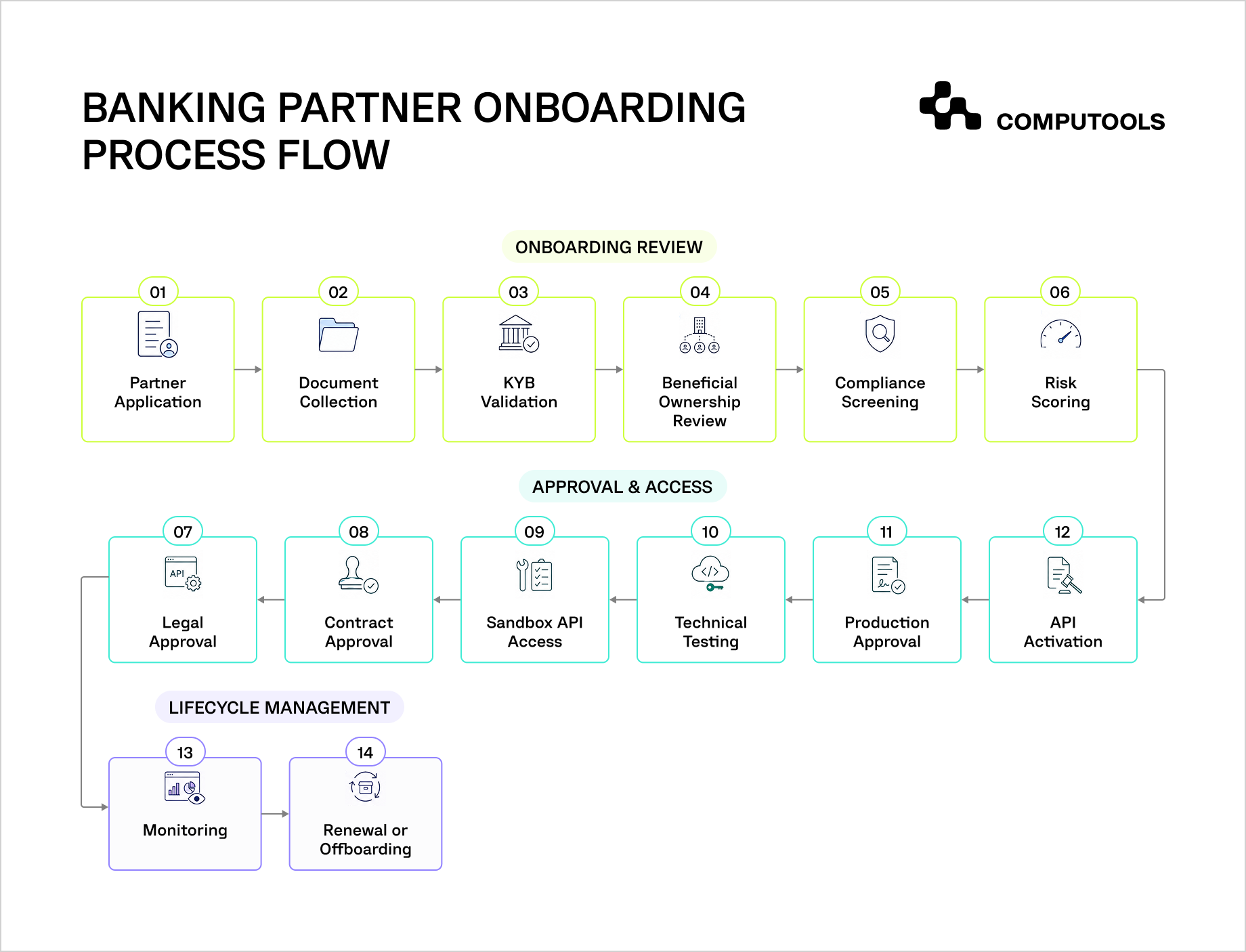

To develop banking partner onboarding software, teams need to define how partner approval, compliance review, API access, risk limits, contracts, and lifecycle governance will work before platform development starts.

1. Define the partner operating model before designing workflows

The first decision is not technical. The bank must define what types of partners it will onboard and what each partner is allowed to do.

The platform should have a simple partner status model. Examples would include: prospect, application started, documents requested, KYB review, compliance review, risk review, contract negotiation, sandbox access, production access, status active, status restricted, status suspended, offboarded. Each status should have associated permissions, tasks, notifications, and audit entries.

From a technical standpoint, this means implementing a workflow engine, role-based access control, partner types, task queues, approval rules, and a partner profile, all with a fully built-out structure. Without this logic, the system will become a document portal without real control. While teams will collect documents faster, approvals will still happen in emails, chats, and follow-up tasks.

For banks, a good partner onboarding platform for banks should have the capability to always and easily answer the following questions. Who is the partner? What products are they asking for? What are the associated risks? Who approved each step and what permissions were granted?

2. Build the data model around KYB, risk, contracts, and access

A banking compliance onboarding platform builds upon the foundation of structured data. Examples of relevant data elements include legal entities, ownership structure, beneficial owners, authorized representatives, licenses, operational country(ies), business model, product(s), expected transaction volume, risk category, contract status, API access level, and monitoring history.

According to the FATF, beneficial ownership information should be adequate, accurate, and continuously updated. Therefore, it should not be captured as loose documents. This data should be structured and linked to a review status, an expiry date, and an audit history.

In practice, KYC and compliance automation for partners should include document classification, required-field validation, expiry alerts, ownership structure capture, sanctions and adverse media screening integrations, and exception handling. The system should also support versioning. A partner’s risk position can change after a new product launch, ownership change, regulatory event, or geography expansion.

If the platform also needs identity verification workflows, Computools’ guide on how to develop an automated KYC verification system explains how document checks, verification logic, compliance automation, integrations, and approval workflows can support regulated onboarding.

The main failure risk here is treating onboarding as a one-time event. In banking ecosystems, partner data should support the full lifecycle. The same records used during onboarding should later support renewals, audits, risk reviews, access changes, and offboarding.

3. Design API onboarding as a controlled activation process

Banking API partner onboarding should consist of multiple stages, as opposed to a singular credential transfer. For example, partner organizations may need initial access to a sandbox environment (as opposed to production), access to a limited set of API functionalities (as opposed to all functionalities), the ability to conduct test transactions (as opposed to full volume operational transactions), and a greater level of engagement to access certain secure API endpoints.

The onboarding infrastructure generally involves API gateway, developer portal, routing and auto provisioning support, OAuth 2.0/OpenID Connect, mutual TLS for high-trust integrations, API scopes, rate limits, separation of environments, webhook support, event logging, API key rotation and versioning. Each API permission should connect back to partner status, contract terms, risk level, and approved products.

For example, a partner approved for account information services should not automatically gain payment initiation access. A card issuing partner should not receive production credentials until compliance approval, contract approval, settlement rules, reconciliation logic, and operational support paths are complete.

In the CardFalcon project, Computools connected operational workflows, partner-bank records, contracts, and backend logic in one environment.

The same principle applies to a banking partner integration platform: API access should not sit outside the business approval process. It should be activated by it.

4. Automate approval workflows without hiding accountability

While partner onboarding workflow automation should minimize the amount of manual work, it shouldn’t detract from accountability. It should offer a way for the partnership team, compliance, legal, risk, product, security, finance, and operations to see where their responsibilities begin/end in the approval process.

It should be able to distinguish between partners and therefore route tasks accordingly based on criteria that will influence the level of risk and the evidence that needs to be provided. This should be coupled with SLA tracking, escalation rules, the maker-checker principle, comments, approval history, and evidence logs.

If workflow automation is too rigid, teams will move exceptions outside the platform. If it is too loose, the bank loses standardization. The right design gives teams configurable rules, but every override should be recorded with the user, reason, timestamp, and affected approval stage.

For banks that need to structure this logic across several departments, Computools’ article on how to develop a banking workflow automation system gives a closer view of approval routing, escalation logic, task control, and operational visibility in regulated banking workflows.

5. Add risk scoring and exposure controls from the start

A bank partner management platform should assign risk levels before activation and update them during the relationship. Risk scoring can include business model, jurisdiction, ownership complexity, product type, transaction volume, regulatory licenses, adverse media results, security posture, operational readiness, and past incidents.

The score should influence practical controls. A high-risk partner may require lower transaction limits, stronger monitoring, shorter review cycles, restricted API scopes, additional evidence, or executive approval. A lower-risk partner may move faster through standard workflows.

This is where fintech partner onboarding software becomes a revenue control layer. Banks often want faster partner activation, but speed without exposure limits can create downstream problems. The platform should define what a partner can do on day one, what must happen before limits increase, and which events trigger suspension or review.

Technically, this requires a rules engine, scoring service, limits service, audit logs, and integrations with transaction monitoring, AML systems, CRM, core banking, payment systems, and reporting tools. Risk should not be a static label hidden in a profile. It should control access, volume, review frequency, and escalation.

For a more detailed view of scoring logic, Computools’ guide on how to develop a risk scoring engine for banking explains how risk indicators, scoring rules, data models, and decision logic can support faster and more consistent banking decisions.

6. Treat security and reliability as revenue protection

When considering banking ecosystem software development, the cybersecurity approach goes beyond protecting against breaches. It safeguards uptime, trust, partner confidence, compliance, and, most importantly, the bottom line. According to IBM’s 2025 Cost of a Data Breach report, the average cost of a single data breach in 2025 was USD 4.4 million. According to Akamai’s 2026 financial services API security research, data breaches and leaks were the most common types of API incidents, with the average cost of API security incidents reaching USD 620,000 per year, per organization.

A secure software architecture encompasses various domains. These include multi-factor authentication, role-based or attribute-based access control, least-privilege access, data protection via encryption both at rest and in transit, secrets management, audit logging, control of API gateways, rate limiting, continuous vulnerability scanning, penetration testing, and secure SDLC, along with data retention and incident response policies.

Reliability also needs design attention. Partner onboarding platforms often connect CRM, KYB providers, AML systems, contract tools, payment infrastructure, developer portals, and core banking systems. When one dependency fails, the platform should degrade safely. Use retries, idempotency keys, queue-based processing, monitoring, backup jobs, disaster recovery plans, and clear operational dashboards.

DORA’s focus on digital operational resilience makes this especially relevant for banks and other financial entities in scope. A partner onboarding system should document who was approved, which critical third-party dependencies support the process, and how incidents are going to be managed.

Partner onboarding should also connect with post-activation monitoring because risk does not end once API access is approved. Computools’ guide on how to build an AML transaction monitoring system explains how alerts, transaction risk scoring, case management, and compliance workflows can support ongoing financial crime control after a partner starts operating.

7. Use AI where it improves decisions

There are a number of ways AI can be helpful in modern automated partner onboarding software. AI document reviews can classify documents, identify incomplete forms, pinpoint expired documents, and review gaps. A smart search feature can help users quickly locate partners, contracts, approvals, and previous decisions. Fraud detection models can analyze partner behavior to identify evidence of onboarding fraud, detect suspicious document patterns, or identify inconsistent business data.

AI can also provide recommendations for the next best action and request additional evidence, case escalation, and enhanced due diligence. Predictive analytics can be used to estimate the completion of the onboarding process, identify bottlenecks during the approval process, and predict the workload for operations.

Pricing intelligence may also be relevant for partner fee models, revenue-sharing structures, API usage tiers, or card program economics. The goal is not dynamic pricing for its own sake. The goal is to make partner economics visible before commercial terms are approved.

AI works best with well-organized data. If any data concerning partners is inconsistent, like tagging documents, approval reasoning, or risk assessment, AI will be of no help. To get the data infrastructure in check, a controlled taxonomy with stable partner statuses and standardized document types, along with decisions that will stand an audit, and loops that give feedback on post-launch outcomes, is needed.

8. Test the platform against operational reality

A banking partnership management software platform must be tested against real approval paths, incomplete applications, duplicate partner records, expired documents, failed KYB checks, API credential errors, contract changes, rejected partners, suspended partners, and offboarding.

Performance testing is also important. Partner onboarding looks like an internal process. However, API calls, document assignment, and screening, along with partner portal traffic can cause problems during launches or large-scale partnership projects.

Role-based testing, workflow, API, and integration testing should all be part of the quality assurance plan. Security testing, audit-log validation, and data migration testing should also be included, along with load testing, which is particularly important for your situation. If the workflow is regulated, user acceptance testing should incorporate compliance, risk, legal, and operations, along with product and partner management teams.

CardFalcon shows the value of building around the full operating process instead of one isolated interface. Computools used an Agile-based delivery approach with short iterations focused on backend business logic, offer and contract flows, partner communication, administrative interfaces, database integration, and deployment infrastructure.

A strong partner lifecycle management for banks setup should also track post-activation events: API usage, failed calls, support tickets, incident history, limit increases, product expansion requests, compliance renewals, ownership changes, and offboarding reasons.

Launch your banking partner onboarding solution within 1–3 months instead of years, accelerating partner activation, compliance, and ecosystem expansion from day one.

Why choose Computools to develop banking partner onboarding software

Computools fits banking partner onboarding projects where partner growth depends on revenue control, operational governance, API access, compliance workflows, and scalable infrastructure. These platforms are rarely limited to partner registration. They need to connect commercial approval, KYB checks, contract status, risk review, API provisioning, partner communication, and post-activation monitoring in one controlled operating flow.

Computools’ experience in financial software development services supports projects where onboarding must connect with payments, customer data, risk controls, compliance workflows, reporting, and transaction-related logic. Our banking software development services are relevant for banks that need secure digital platforms, API integrations, fraud detection, and modernization around existing banking infrastructure. Our fintech software development experience supports integrations with KYC/AML providers, third-party fintech services, open banking environments, real-time dashboards, and cloud-native systems.

For the product layer, Computools’ web development services can support partner portals, internal admin panels, compliance dashboards, risk dashboards, contract workspaces, and developer-facing interfaces. This matters because each user group needs a different view of the same partner record.

Computools’ AI development and data engineering capabilities make the platform more useful, offering document classification, missing-data detection, smart search across partner records, risk signal review, onboarding bottleneck analysis, and AI-assisted support for partners. Our cybersecurity services strengthen access control, API protection, auditability, and secure delivery.

The CardFalcon project shows the same delivery logic in a banking context: fragmented partner-bank workflows were moved into a structured digital environment with backend logic, controlled data storage, operational interfaces, CRM-related functionality, and containerized deployment. That is the level of system thinking needed to develop banking partner onboarding software that supports ecosystem growth without losing control.

The main value is that Computools can connect the platform to the business system around partner growth. Banks get a way to reduce manual workload, speed up partner activation, protect API access, improve compliance evidence, control risk exposure, and track the operational blockers that delay revenue.

Final thoughts

Banks cannot scale partnering ecosystems using email approvals, shared folders, manual KYB checks, and fragmented API access. While these methods may accommodate the initial partners, they will inevitably fail when the bank has to manage a variety of partners, products, contractual agreements, risk levels, jurisdictions, and integration models.

Digital onboarding for banking partners should enable teams to employ a single, controlled pathway with due diligence, contracting, risk assessment, accessing sandboxes, going live, ongoing partner monitoring, renewals, and offboarding. The platform should also allow team members to see the current stage of partner onboarding, approval blockers, missing documents, active API scopes, and the risks to be addressed.

The strongest platforms connect business rules with technical controls. Partner status should influence API access. Risk level should influence limits and review frequency. Contract status should block or approve production access. Compliance evidence should remain audit-ready after onboarding, not disappear into folders.

To develop banking partner onboarding software that works at an ecosystem scale, banks need to design it as an operational control layer. It must support revenue activation, compliance visibility, API governance, partner lifecycle management, and scalable integrations from the start.

Computools

Software Solutions

Computools is an IT consulting and software development company that delivers innovative solutions to help businesses unlock tomorrow.